I Found That No Currency in History Has Ever Tracked What It Was Supposed To

The Money Series, Part 3: The case for a currency anchored to the one thing that cannot be printed.

This is the third piece in a series, and it builds directly on parts 1 and 2, so if you have not read them yet, this is a good moment to go back and start there. What follows will make more sense with that foundation, though here is the short version if you would rather keep going: money was invented to solve a trust problem that breaks down once communities grow too large for anyone to keep track of who pulled their weight, and every solution humans have tried since, shells, precious metals, coins, paper, digital, has failed in exactly the same way. The representation drifted from the thing it was meant to represent.

That pattern raises a question worth sitting with for a moment before trying to answer it. Two different things are riding on the answer. If the premise is wrong, everything the rest of this series builds on top of it is wrong too, no matter how carefully argued, the same way a cracked foundation eventually shows up in every floor built above it. But if the premise is right, the stakes run past this series entirely: it means the basic understanding of where economic value comes from, the one almost everyone currently operates on, has been miscalibrated the whole time. We think the value lives in the object itself, the gold, the oil, the television. It does not.

The question is this: what has every form of money been standing in for? Every version of money that has ever existed was a substitution, a stand-in for something that cannot change hands on its own. You cannot hand someone an hour of your life the way you can hand them a loaf of bread. Time has no physical form. It cannot be touched, stored, or passed across a table, so every monetary system in history has had to choose some physical or digital stand-in instead. Gold was chosen because it was scarce and hard to fake. Paper was chosen because it was portable. Digital ledgers were chosen because they are fast and cheap to transfer. Each substitution solved a real problem. Each one also introduced a new vulnerability: the gap between the representation and the reality it was supposed to track.

This creates an amazing opportunity. What if we used the thing that everything else was a substitute for, human time itself, as the thing that backs the currency’s value?

Value Has Never Lived in the Object

To understand why human time is the foundation of the economy, start with the animal kingdom, not because animals lack the mental tools, but because watching where they stop short shows you exactly what’s missing.

A wolf does not assign value to an oil deposit. A crow has no use for a vein of copper ore. The natural world is full of minerals, fossil fuels, and rare earth elements that existed for billions of years before any economy existed to price them. None of it had value in any economic sense, and the reason is not that animals lack the cognitive tools involved. Crows use tools. Squirrels plan ahead for winters that have not arrived. Wolves track which packmate pulled their weight on a hunt. Animals imagine, plan, and remember favors well enough to get by (1 & 2).

Here is where they stop short. Animals can live a particular act of reciprocity between two individuals, but none has ever been shown to abstract it into something a stranger could honor: a token, a claim, a record that means something to a third party who was never part of the original exchange. A wolf that recognizes a packmate’s effort has no way to turn that recognition into something a wolf from a different pack would accept. The reciprocity stays bound to the two animals who lived it. That single missing step, turning a lived relationship into a transferable claim, is the entire reason resources sitting in the ground never accumulate value on their own (3).

None of this happens for free, including the thinking itself. Abstracting a relationship into something a stranger could honor, recognizing scarcity, working out a fair trade: every one of those is an act of cognition, and cognition draws on the same finite hours as digging, building, or hauling. That is part of why time is the resource being tracked in this argument, even in the moments when nothing physical is happening, yet, when what is occurring is a person standing still, working something out in their head.

Here is what that looks like in practice. A deer standing in the woods has no economic value. It does nothing for anyone simply by existing out there. The moment a hunter spends time tracking and killing it, the deer becomes something, but it is still just a carcass, not meat anyone can use. Nobody driving past a deer killed on the side of the road thinks there is three hundred dollars sitting on the shoulder, and they are right not to. The carcass alone is worth nothing. If the hunter is unwilling or unable to butcher it himself, someone else must spend their time doing it, and that time is exactly what turns a carcass into something a kitchen can use.

Notice exactly what the hunter is paying for when he hands the butcher money instead of doing the work himself. He is not really paying for meat. He is paying to get his own time back, spending dollars specifically to avoid spending the hours and time it would have taken to learn the skill that butchering the deer would have cost him. Every step from there, cutting, packaging, transporting, and selling, is another increment of human time being added, and the final price on a package of venison is that accumulated time, stacked and priced.

This scales far beyond a single deer. In theory, if you own land, the raw materials for almost everything around you are already there somewhere in the ground beneath it: the silicon in a computer chip, the metals in a couch frame, the elements that make a television work. Nothing stops you from going out and finding these materials yourself, at no monetary cost, since nobody owns the right to charge you for digging in your own backyard. But finding and extracting them still costs you something real: your own time. And even setting that cost aside, doing it yourself would be wildly inefficient.

Learning to extract and work metal, to fabricate semiconductors, and the dozens of other specialized skills it would take to turn raw ore and sand into a working television would consume years, probably decades, of a single person’s life. Time that person could have spent on almost anything else, including what they are skilled at. That assumes one person could even do it alone, and they could not. A working television is not a single skill mastered by one mind. It is the output of mining operations, refineries, fabrication plants, and supply chains built by thousands of people over decades, none of whom could have built the whole thing alone. No individual lifetime, however long or however skilled, was ever going to be enough on its own.

This means there is a technical sense in which the materials inside a television are free. What you are paying for, every time you buy one instead of building it yourself, is everyone else’s accumulated time and specialized knowledge, packaged and compressed into a price, so that you never have to spend your own decades reinventing what they already know how to do.

Notice something else hiding underneath all of this. The very idea that this land is yours, and not someone else’s, is itself a human invention. Nature does not recognize property lines. No tree, no river, no deposit of ore in the ground carries any natural marker saying who is allowed to claim it. A deed, a title, a fenced boundary, all of it is enforceable only because enough people agree to treat it as real and are willing to back that agreement up.

Now take the thought experiment all the way: remove not just the agreement, but every human being who could ever make one. No owner, no claimant, no one even thinking about the land at all. What is left is exactly what was there before any human existed to want anything from it: just ground, belonging to no one, valuable to no one, because value was never sitting in the dirt waiting to be found. Even ownership itself runs on the same fuel as everything else in this section. It exists because humans spent time building the idea, agreeing to it, and enforcing it. Take the human time and the human agreement out of the equation, and the concept of “mine” disappears along with the value, because there was never anyone left to assign either one.

This is the first layer and the foundational one. Value requires human time to be spent, imagining, hunting, building, learning, owning, and exchanging. That is not a poetic observation. It is the structural premise on which the entire economy rests.

The Same Substance, A Completely Different Price

This same mechanism explains something that looks, at first, like a contradiction: a substance can sit completely unchanged while its value swings from a nuisance to a fortune, or from a fortune to almost nothing.

For much of the eighteen hundreds in Pennsylvania, crude oil seeping up through the ground was not valuable. It was a problem. Farmers avoided land where it surfaced because crops would not grow there. Miners drilling for salt water kept hitting oil that contaminated their wells, and they treated it as a nuisance to be cleared away, not a resource worth keeping. The oil had not changed. What changed, starting in the late 1840s, was that someone spent the time figuring out what that oil could become, and within a decade, the same substance that had been ruining wells and farmland was the foundation of an entirely new industry (4 & 5).

The same reversal happens in the other direction, too. For generations, sperm whale oil was among the most prized lamp fuels in the world, valued specifically for the clean, bright light it produced. For households that could afford it, nothing else available at the time delivered the same quality of light without the foul smell and heavy smoke of cheaper alternatives. People hunted whales across entire oceans, at real danger to their lives, for the oil inside a single whale’s head. That oil is largely irrelevant today. Nobody hunts whales for lamp fuel anymore, and the oil itself did not change in any way to cause that. It is chemically identical to what it always was. What changed is that kerosene, derived from petroleum, delivered the same clean, bright light at a price ordinary households could afford. Once that happened, the premium on whale oil did not gradually shrink. It simply stopped making sense. Nobody in their right mind pays more for a product that does the same job as a cheaper one sitting right next to it on the shelf. Decades of accumulated value, built entirely on being the best available path to something people genuinely needed, collapsed the moment a better path opened (6 & 7).

Notice what both prove together. The oil in Pennsylvania and the oil in a sperm whale’s head were never valuable or worthless because of anything intrinsic to the material. Someone could object that whale oil’s value came from scarcity rather than need, since most families could never afford to burn it regularly. But scarcity is not a separate explanation here. Whale oil was scarce precisely because getting it cost a dangerous, monthslong voyage for a barrel pulled from a single animal’s head. The scarcity was the time cost, measured in risk and danger rather than hours alone. The substance is the constant. Human time, knowledge, danger, and need are the variables that have ever moved (7).

This is also why people rarely feel like they are paying for human time directly, even though they always are. Nobody buying a piece of furniture is thinking about the logger’s morning or the mill worker’s shift. They are looking at a price tag. But that price tag exists only because someone, somewhere, spent real human time making the thing available.

It is worth being precise about what would prove this wrong, because a claim that cannot fail in principle is not worth much. The test is not whether an animal shows cognition. It clearly does, as the tool use, planning, and reciprocity tracking described above already shows. The test is narrower and more specific: has any animal, anywhere, been shown to take a lived relationship and abstract it into a token a complete stranger would honor? Not a memory two animals share. A claim a third party, who was never part of the original exchange, would accept as real. No animal has ever been shown to make that leap.

Humans crossed that threshold, but not as early or as automatically as it might seem. Even prehistoric humans, who undoubtedly built and used tools, did not operate anything resembling the economic systems this argument is describing. Tool use by itself was never the threshold. What changed, and changed only after long stretches of human history, was the further step of abstracting a contribution into something that could be tracked, stored, and eventually handed to a total stranger as proof that it had occurred. This argument would be falsified by demonstrating that leap occurring outside of human cognition: a system, anywhere in nature, where a contribution gets abstracted into something transferable and honored by a party who was never part of the original relationship at all.

This explains why value exists at all. It does not yet explain why two things that cost the same amount of human time can sell for wildly different prices, and that gap is where the next layer begins.

Why Price and Value Are Not the Same Thing

Layer one exists to answer one question: where does value come from? The answer was human time, knowledge, danger, and need, and the proof was a substance that swung from worthless to a fortune and back while never changing at all.

Layer two exists because of something layer one does not fully explain on its own. Value and price are not the same thing, and most of what gets written about economics treats them as if they were. Given that value requires human time and cognition to exist at all, how does the market decide what something costs? Sometimes the price tracks the value closely. Sometimes it does not, and the gap between them is not a flaw in the theory. It is the next thing the theory must explain.

For most of what gets bought and sold, the answer tracks layer one closely. Competition keeps price pinned near whatever it costs, in time and effort, to bring the next unit to market. A computer’s price has very little to do with how much value it brings to the person buying it, and almost everything to do with what it costs, in time and labor, to get the raw materials from nothing to a finished product, plus whatever margin the market will allow once every competitor is trying to undercut every other one. Water works the same way for a different reason: demand for it is not optional, but because supply is competitive and expandable, price still gets disciplined down toward the cost of delivering it, not pushed up toward what people would pay rather than go without.

Aluminum shows how far that discipline reaches, even against the wishes of the people holding the asset. In 1852, aluminum cost nearly twice as much as gold, ounce for ounce, expensive enough that Napoleon III reserved aluminum cutlery for his most honored guests while everyone else made do with gold. The metal had not gotten any rarer or any less useful by 1886. What changed was that two chemists, working independently, found a cheap way to extract it from its ore. Production time collapsed, and the price collapsed with it, falling more than eighty percent within five years of the process being commercialized, a drop so steep that no aluminum holder’s preference for the old price could slow it down. Everyone of them would have preferred the price to stay where it was. It did not matter. Once competing producers could make aluminum cheaply, none of them could afford to hold the old price, because someone else would always undercut them. The price was never protecting the value of the metal. It was tracking the human time it cost to free the metal from the rock, and the moment that time collapsed, so did everything built on top of it (8, 9, 10 &11).

Diamonds and gold sit on the other end of that spectrum, and the reason is not that they escape human time. It is because their supply does not face the same competitive pressure. The labor and processing that goes into a diamond is real, but it is nowhere near enough, on its own, to explain what people pay for one. The rest of that price comes from scarcity that cannot be competed away, and from enough people wanting one badly enough, and believing enough other people want one too, that they are willing to pay far more than the stone’s production ever cost. Gold has a similar effect on a larger scale: a meaningful share of all the gold ever mined sits in vaults and central bank reserves, held specifically because it is gold, not because anyone is about to use it for anything.

None of this contradicts layer one. A diamond’s premium still requires a human mind to want it in the first place, just as every example in this article has. What it shows is that price and production time can come apart once competition stops disciplining the gap between them, and that gap gets filled by something else entirely: scarcity, status, and belief, not additional time spent making the thing.

The One Thing You Cannot Print

Here is what makes human time different from every proxy ever used to represent it.

You cannot manufacture it. You cannot expand the supply on command. No government decree, no technological innovation, no financial engineering adds a single hour to the total stock of human hours alive in the population at any given moment. The only way the total grows is the slow way: more people being born, or the same people becoming able to accomplish more with the hours they already have, which is what productivity measures. No single person ever gets more than twenty-four hours in a day, and no one ever has, in any era of recorded history. Both legitimate growth channels, population and productivity, are slow and hard to hide. Nobody can secretly double a country’s population overnight, and nobody can secretly make an entire workforce twice as productive without it showing up, visibly, in how goods get made and how long things take.

This is not true of precious metals. It was mined in far greater quantities when Spain discovered silver in the Americas, and it can be mined again if new deposits are discovered. It is not true of paper currency: the supply can be expanded at the cost of a printing press, or today at the cost of a keystroke. It is not true of any commodity or any government-issued token. None of those substitutions ever had to clear the bar; human time clears automatically: visible, gradual change, with no way to manufacture a sudden jump that nobody could see coming.

An hour of human labor has always been an hour of human labor, and it is worth being precise about what that means and what it does not. A worker in 1910 digging a foundation by hand spent an hour of real physical strain that no one alive today, sitting at the controls of an excavator, would call equivalent. The 1910 hour was harder. The hour today produces more. Those two facts do not cancel out, and they are not supposed to. The tools, the knowledge, and the infrastructure built since 1910 changed what an hour can produce and how much that hour costs the body and mind producing it, but those changes ran in different directions for different reasons, and neither one is what determined the hour’s claim on the economy.

Here is the part that is easy to miss. More output does not mean more claim on the economy, and less physical strain does not mean less claim either. If everyone’s hour now produces more while costing less effort, then more of everything exists, and people work harder less often, but everyone else’s hour changed by roughly the same amount, so the share of the total economy that any single hour can claim does not move just because the ceiling above it rose or the strain beneath it fell. Productivity raised what an hour can build and lowered what it costs the body to build it.

Neither one touched what that hour is worth relative to every other hour being spent at the same time. The hour itself, as a fixed unit of time a person commits and can never get back, has not changed at all, and neither has its monetary claim on the whole economy, even while everything around it, what it produces and what it costs to produce, has moved in opposite directions at once. That is the specific claim this series is building toward: not just that value comes from time, but that the dollar value an hour commands has remained nearly flat for a hundred years, while the official numbers tell a different story. Output moved. Effort moved. The monetary claim did not.

That unchanging quality is the anchor that every substitution has been trying to approximate. None of them got there. That same unchanging quality is also where the trouble starts today. We treat productivity gains as growth, as the economy genuinely getting bigger and richer, when this framework says something narrower is happening: an hour can build more, but it is not commanding any more of the economy than it ever did. Calling that growth is not wrong about the output. It is wrong about what the output means for the value of an hour, and that confusion lies beneath every modern conversation about wages falling behind, productivity rising, and people feeling like the gains never reached them.

What the Numbers Show When You Apply the Drift

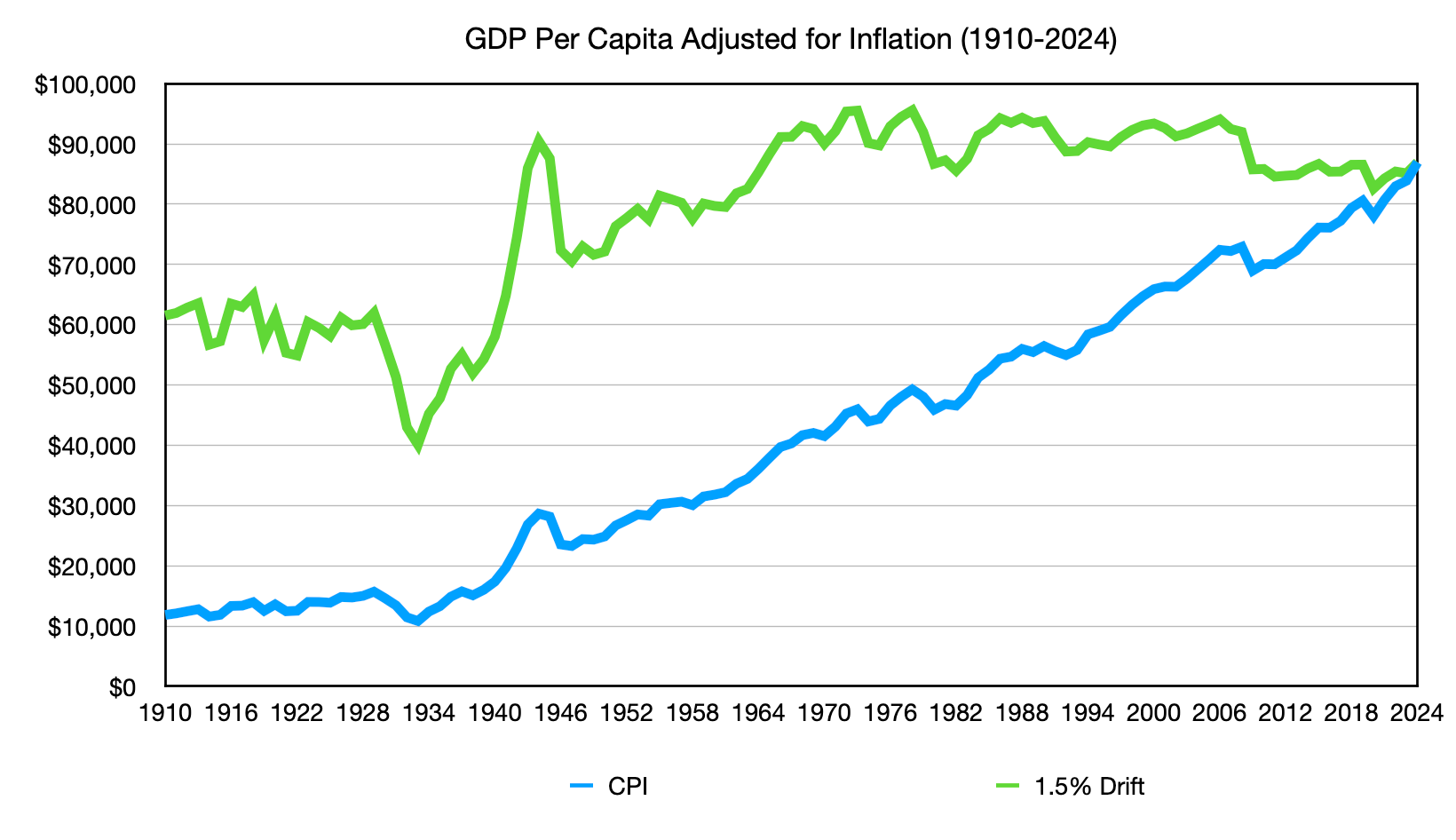

There is a way to test whether this framing has merit, and it is worth looking at the data directly.

If human time is the actual anchor of economic value, then the monetary claim one human hour generates against the total economy should stay relatively stable across long time horizons. Productivity changes what an hour produces. It does not change the underlying claim that hour makes. To genuinely grow the monetary value of the economy, you need more hours, which means more people, not more output squeezed from the same number of hours.

This means the prediction is specific enough to be tested and specific enough to be wrong. If you look at GDP per capita using official inflation figures, the numbers should look like an hour of human time has become dramatically more valuable over the past century, since productivity gains get folded into the price level rather than separated out from it. That apparent gain is not what this framework predicts is happening. It predicts something closer to flat, once productivity is properly accounted for, separate from any real growth in the underlying claim an hour makes on the economy.

Here is what the data shows. Under official CPI adjustment, GDP per capita in the United States grew from roughly $12,500 in 1910 to nearly $87,000 today, an increase of almost 600%. That is the inflated, productivity-conflated number this framework predicted you would see if you used CPI directly. Adjust the same GDP figures using the gross inflation rate this publication has laid out elsewhere, roughly one and a half percentage points higher than CPI captures each year, compounded across the full century, and GDP per capita shows an increase of roughly forty percent over the same period. Forty percent over more than a hundred years is close to what population growth and modest productivity gains alone would predict, without each hour somehow having to be worth six times as much (12, Full methodology included).

This does not prove the framework. A single data point, run through one adjustment method, is a consistency check, not a verdict, and it deserves to be treated as exactly that. The sequence matters here, and honesty about it matters more. The foundation of this work started with a different observation entirely: that human time is the main currency of the economy, the thing every monetary system has always been trying to represent. That insight came before any inflation work was done. When the 1.5% drift was identified through a separate line of analysis, documented elsewhere in this publication, applying it was not only consistent with the human time framework. It was the moment the two lines of reasoning clicked together. An economy whose real per capita output has stayed nearly flat for a century is exactly what you would expect to find if human time is the anchor and the drift is real. Two independent lines of reasoning converging on the same result is not proof. But it is the right kind of result to find, and it is the kind of convergence that is difficult to dismiss as a coincidence. The full calculation behind the gross inflation adjustment, including its sources and its limits, is laid out in detail elsewhere in this publication for anyone who wants to follow the math themselves rather than take the conclusion on faith.

The Standard Every Currency Has Failed to Meet

Here is where this series has been building towards this whole time.

Every previous attempt reached for a proxy instead, gold, paper, a ledger entry, because nothing else was available to track human time directly at the scale a modern economy requires. Most of the banking system today already runs on a digital ledger, and that alone never solved the problem, since a ledger that only one party can see inside is just the vault problem from before, digitized. What has changed is narrower and newer: the emergence of ledger systems that nobody single party controls, verifiable by anyone with access to them, rather than being trusted on an issuer’s word. Blockchain is the clearest example, though it remains unproven at the scale a real currency would require (13).

Whether that specific technology or something built on the same principle ends up doing the job, the capability it points toward, a ledger no single party controls, did not exist for any previous generation that tried to solve this problem. Something as it exists now. What it would take to build that system is a separate question this piece does not answer, but the constraint that forced every past substitution to reach for a worse proxy is no longer the obstacle it once was. Nothing else in the history this series has covered, not shells, not gold, not paper, not a ledger controlled by a single issuer, has ever met the bar of being anchored to human time itself.

But anchoring alone was never the whole standard, and pretending otherwise would repeat the exact mistake this series has spent two pieces documenting. Gold backing never failed because gold was the wrong metal. It failed because no one outside the vault could check, in the moment, whether the receipts in circulation still matched the gold sitting inside it. An anchor that cannot be checked is not much better than no anchor at all, since the checking is what makes the anchor mean anything to a stranger who was never in the room when the promise was made.

What this piece does give you is the standard itself, stated plainly enough to build toward. A currency anchored to human time is not a new kind of trust. It is the same shift money has always made, trusting the token instead of the stranger holding it, finally pointed at something the token can keep faith with. Get that right, and a currency stops asking anyone to trust a government’s promise, a central bank’s discipline, or a stranger’s word. It only asks them to trust that the substitution is honest and will still hold up the next time they go to spend it, which is a question that can be checked rather than simply believed. That trust is what lets goods and services move freely between people who will never meet and have no reason to know each other’s names, the same problem this series opened with in Part 1, finally answered instead of just patched over.

This is the conceptual foundation of the Novack Equilibrium Theory. We have spent thousands of years building representations that drift, and failed every time. The thing human time represents cannot drift. What remains is building something that lets everyone check that it hasn’t.

The Cost of Getting This Wrong

You might reasonably ask: this is interesting history and economic philosophy, but what does it have to do with the economy I am living in right now?

The answer is direct. If money has been drifting away from its anchor in human time, the measurements we use to track economic progress have been recording that drift as prosperity. Wages look like they have grown. Living standards appear to have improved. The economy appears to have expanded dramatically over the last century.

Some of that is real. Productivity gains have genuinely made life better in measurable ways. But some of it is the ruler shrinking while we report the distance as growth. When you use a standard that drifts as your measure of progress, you cannot distinguish between the two.

That is not a small problem. Take a pension calculated decades ago, built on an assumption about what a dollar would still be worth by the time someone retired. If the dollar has been drifting the entire time, that pension was never calculated against a stable target. It was calculated against a target that was already quietly shrinking, and nobody designing it could have known by how much. The same blind spot lies beneath wage negotiations, government budgets, and interest rate decisions: each is calibrated against a metric that may conflate genuine productivity gains with the quiet erosion of what each dollar represents.

The rest of the NETs work is an attempt to separate those two things and see what the economy looks like when they are held apart.

That work starts with understanding what money was always supposed to be. It was supposed to be a faithful record of the hours humans spend building things, growing things, providing services, and caring for each other. It was never supposed to drift.

We built it to track us. Somewhere along the way, we lost track of it.

Source and Methods

1. Delgado, M. M., Nicholas, M., Petrie, D. J., & Jacobs, L. F. (2014). Fox squirrels match food assessment and cache effort to value and scarcity. PLOS ONE, 9(3), Article e0092892. https://doi.org/10.1371/journal.pone.0092892

2. Mech, L. D. (2007). Possible use of foresight, understanding, and planning by wolves hunting muskoxen. Arctic, 60(2), 145–149. https://doi.org/10.14430/arctic239

3. Wimpenny, J. H., Weir, A. A. S., Clayton, L., Rutz, C., & Kacelnik, A. (2009). Cognitive processes associated with sequential tool use in New Caledonian crows. PLOS ONE, 4(8), Article e6471. https://doi.org/10.1371/journal.pone.0006471

4. American Chemical Society. (2009). The development of the Pennsylvania oil industry [National Historic Chemical Landmark]. https://www.acs.org/education/whatischemistry/landmarks/pennsylvaniaoilindustry.html

5. American Society of Mechanical Engineers. (December 11, 2024.). Drake’s oil well started a revolution [ASME Engineering Landmark]. https://www.asme.org/topics-resources/content/drake%E2%80%99s-oil-well-started-a-revolution

6. American Oil and Gas Historical Society. (n.d.). Camphene to kerosene lamps. https://aoghs.org/products/camphene-to-kerosene-lamps

7. Nordhaus, W. D. (1996). Do real-output and real-wage measures capture reality? The history of lighting suggests not. In R. J. Gordon & Z. Griliches (Eds.), The economics of new goods (pp. 27–70). University of Chicago Press.

8. American Chemical Society. (1997). Hall process production and commercialization of aluminum [National Historic Chemical Landmark]. https://www.acs.org/education/whatischemistry/landmarks/aluminumprocess.html

9. Geoscience Australia. (May 14, 2025.). Aluminium. Australian Government. https://www.ga.gov.au/education/minerals-energy/australian-mineral-facts/aluminium

10. Science History Institute. (n.d.). Paul Héroult and Charles Martin Hall. https://www.sciencehistory.org/education/scientific-biographies/paul-heroult-and-charles-m-hall

11. NPR. (2019, December 5). A short history of aluminum, from precious metal to beer can. https://www.npr.org/2019/12/05/785099705/aluminums-strange-journey-from-precious-metal-to-beer-can

12. Full GDP Per Capital Methodology

a. GDP per capita figures are calculated by dividing nominal GDP by U.S. population for each year. Nominal GDP from 1790 to 2023 is sourced from MeasuringWorth; 2024 nominal GDP is sourced from FRED. Population from 1820 to 2022 is sourced from the Maddison Project Database (Bolt and van Zanden, 2024); 2023 and 2024 population figures are sourced from U.S. Census Bureau Vintage 2024 estimates. Inflation adjustment for 1790 to 1912 uses year-over-year changes derived from the Warren and Pearson wholesale price index, as compiled in Historical Statistics of the United States, 1789–1945 (U.S. Bureau of the Census, 1949). The 1913 splice year is indexed to zero inflation, consistent with negligible price movement at that boundary. Inflation adjustment from 1913 to 2024 uses annual average CPI-U data from the Bureau of Labor Statistics. The gross inflation adjustment adds 1.5 percentage points annually to the official CPI figure, compounded across the full period. The methodology and evidentiary basis for the 1.5% drift figure are documented separately in the NETs technical series.

b. Bolt, J., & van Zanden, J. L. (2024). Maddison style estimates of the evolution of the world economy: A new 2023 update. Journal of Economic Surveys, 1–

c. U.S. Census Bureau. (2024, December 19). National and state population estimates: Vintage 2024 [Press kit]. U.S. Department of Commerce. https://www.census.gov/newsroom/press-kits/2024/national-state-population-estimates.html

d. Federal Reserve Bank of St. Louis. (n.d.). Gross domestic product [GDP]. FRED. https://fred.stlouisfed.org/series/GDP

e. Williamson, S. H. (2025). What was the U.S. GDP then? MeasuringWorth. https://www.measuringworth.org/usgdp/

f. U.S. Bureau of the Census. (1949). Historical statistics of the United States, 1789–1945: A supplement to the Statistical Abstract of the United States (Chapter L: Price Indexes). U.S. Department of Commerce. https://www2.census.gov/library/publications/1949/compendia/hist_stats_1789-1945/hist_stats_1789-1945-chL.pdf

g. Note: The Warren and Pearson wholesale price index (Series L2–L3) is the source for pre-1913 inflation data in this analysis. Warren and Pearson’s original data appear in: Warren, G. F., & Pearson, F. A. (1933). Prices. John Wiley and Sons.

h. U.S. Bureau of Labor Statistics. (2024). Consumer Price Index, all urban consumers (CPI-U), U.S. city average, all items: Annual averages, 1913–2024. U.S. Department of Labor. https://www.bls.gov/cpi/tables/historical-cpi-u-201709.pdf

13. Nakamoto, S. (2008). Bitcoin: A peer-to-peer electronic cash system. https://bitcoin.org/bitcoin.pdf

Author: Kyle Novack

June 30, 2026

A Monumental Venture, LLC: research project (Novack Equilibrium Theory – NETs)

Attribution Required: © 2025–2026 Kyle Novack / Monumental Venture, LLC. For educational use with credit; commercial use requires permission. Full details in linked PDFs.